Short-term guaranteed investment certificates (GICs) are simply GICs with terms of less than one year – anything from 30 to 364 days. Financial institutions will guarantee the principal (the original investment) plus an advertised rate of interest, but the shorter the term, the lower the interest rate.

Why invest in a short-term GIC?

Short-term GICs are appropriate if you are looking to invest a lump sum of money for a short period of time and want to guarantee your principal. Let’s say you are planning on making a major purchase in the near future, such as a car or a home. A short-term GIC allows you to earn some interest on your savings with the guarantee that the principal will be returned to you as well. Compare this with an investment in the stock market, where the potential for a loss of principal exists, and you can see why some investors include short-term GICs in their portfolio.

Short-term GICs also are considered reasonably “liquid” because they mature so quickly. In other words, you are not locking your money in for an extended period of time, like you would with long-term GICs. This is smart for investors, because it allows them to reinvest the money somewhere else in short order. For instance, if interest rates start to go up, an investor in a short-term GIC can take advantage of the better rates when their GIC matures.

Case Study: Increasing interest rate environment

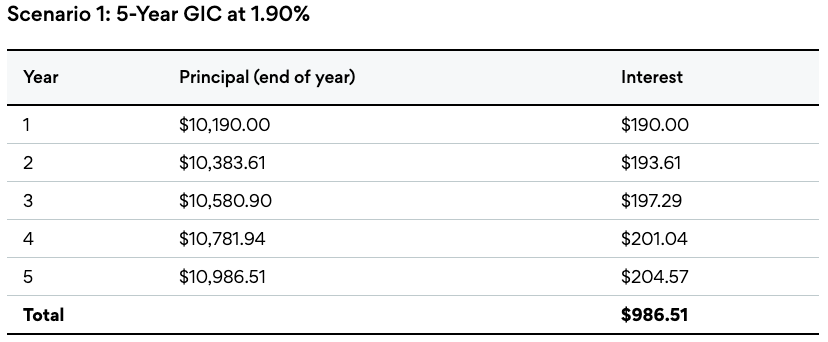

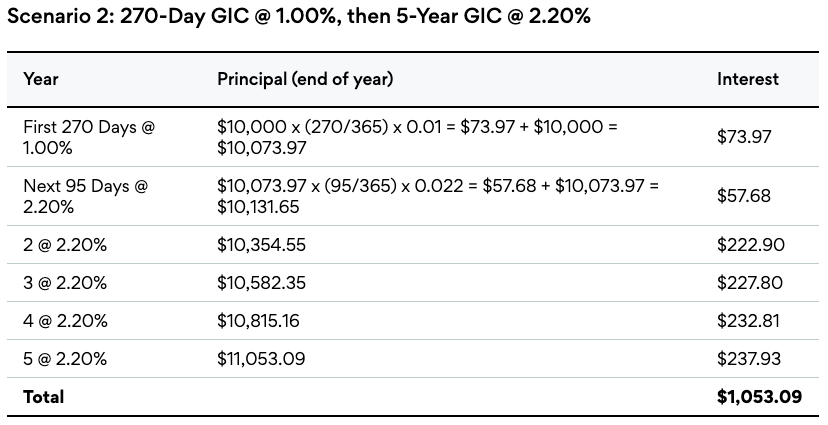

Let’s say John is looking to invest $10,000 and is considering either a 270-day GIC @ 1.00% or a 5-year GIC @ 1.90%. He decides to go for the 270-day GIC, because he suspects interest rates may rise within the next year – and he’s right. By the end of the 270-day term, GIC rates start climbing, reaching 2.20% for 5-year terms.

As you can see, John’s decision to start investing in a short-term GIC first, thereby giving him the ability to reinvest his money sooner, helped him earn an additional $66.58 in interest over the life of his investments.

Features and restrictions of short-term GICs

There are a number of features and restrictions to consider, before investing in short-term GICs:

- Short-term GICs are better than long-term GICs, if you think interest rates will rise in the near future, because you can reinvest your earnings sooner.

- However, you run the risk of interest rates going down, by not locking into current long-term GIC rates.

- If having access to your money is a priority for you, a short-term and/or cashable GIC would be a preferable investment.

- Depending on the interest rates, though, a high interest savings account can sometimes be a better option. For example, BMO’s Smart Saver account currently pays 1.05%1, while their 270-day GIC only pays 1.00%.

- If you’re looking at high interest savings accounts, though, check the transaction fees. In the case of the BMO account, every withdrawal is subject to a $5.00 fee, which would take a bite (and more) out of your interest

Comments

0 comments

Article is closed for comments.